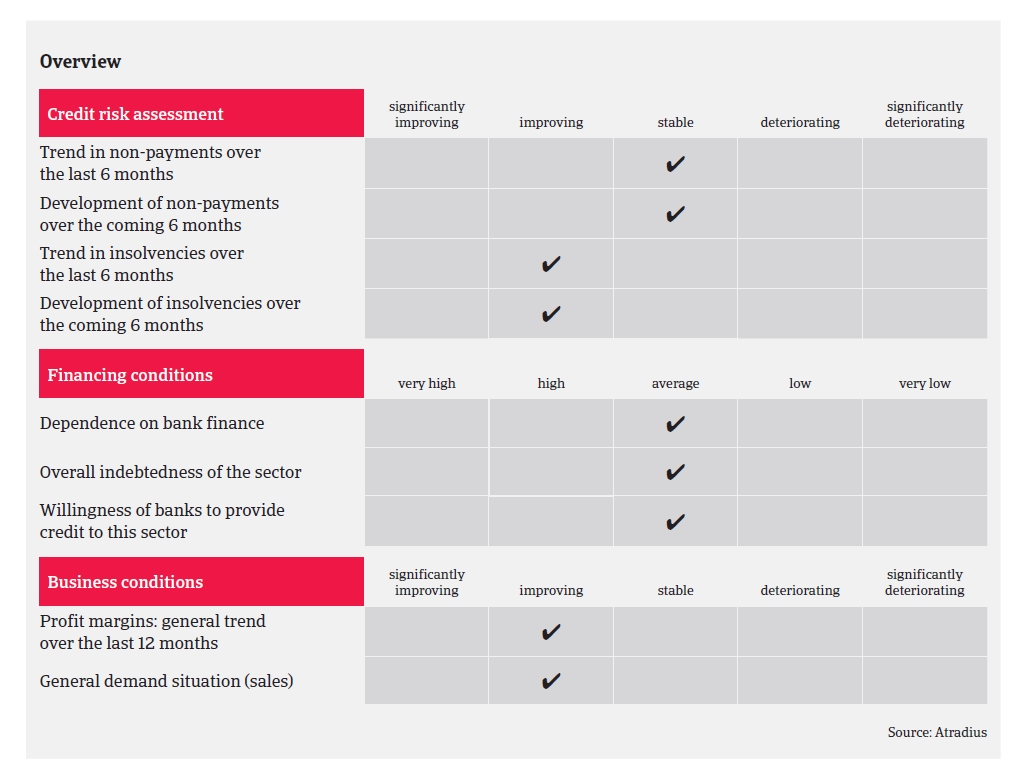

Profit margins of machinery businesses rebounded in 2016 and are expected to improve further, but competition remains strong in the domestic market.

- Competition remains strong in the domestic market

- Payment duration is 100 days on average

- Insolvencies are expected to decrease again in 2017

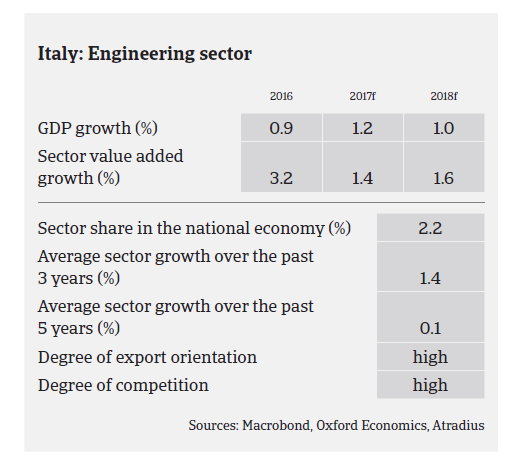

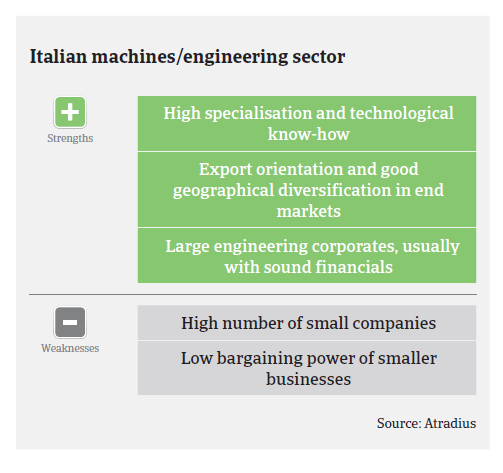

The Italian machines/engineering sector has proved to be relatively resilient during the downturn of Italy´s economic performance after 2008, due to its export orientation, high specialisation and added value products in precision mechanics. Value added growth of the industry increased above 3% in 2016, and is expected to rise further in 2017 and 2018, by about 1.5% annually.

As in previous years, competition remains strong in the domestic market, especially among small and medium-sized machinery companies dependent on construction businesses. While domestic capital investment growth has picked up again since 2016, the construction and road machinery segment performance is still hampered by the slow construction rebound in Italy. The earthmoving machinery segment is highly dependent on public works and therefore exposed to structurally slow payments by public entities. At the same time, demand for machinery related to the oil and gas sector remains subdued.

In contrast, the machinery segment dependent on the manufacturing sector continues to benefit from export growth and increased domestic market demand (especially from the automotive and food sectors). Larger and more diversified machinery companies and export-oriented SMEs are expected to improve performance and cash generation. Overall, profit margins of Italian machinery businesses rebounded in 2016 and are expected to improve further in 2017.

Payment duration in the Italian machinery sector is 100 days on average. Payment experience has been good over the past two years, and the level of protracted payments is low. Non-payment notifications have been stable over the last 12 months, and are expected to remain low in the coming months. The number of insolvencies in the machinery sector is relatively low. Machinery insolvencies are expected to decrease further in 2017, by about 5%.

Our underwriting approach remains generally open, especially for larger businesses and niche export-focused subsectors (e.g. high precision mechanical works). Those businesses usually show solid financials and a good liquidity profile. However, we are still more cautious about companies operating in still difficult end-sectors (e.g. construction) and which are dependent on public entities. We closely monitor machinery businesses which produce components for the oil and gas sector, as investments in this industry have deteriorated over the past two years due to lower energy prices.

Relaterte dokumenter

1.2MB PDF